The global ferrous scrap market showed mixed sentiments this week. Turkiye’s imported scrap prices, on one hand, moved up by $8-10/t w-o-w. On the other hand, Pakistan’s imported scrap market was muted amid the currency crisis and Bangladesh market was quiet amid continuing LC issues. Indian steel industry awaited budget announcement and therefore, fewer activities were seen throughout the week. Japan’s and Vietnam’s scrap market remained steady.

Turkiye ferrous scrap market turns active: Global imported scrap market leader, Turkiye, continued booking throughout this week. A bunch of deals were concluded out of which two were from the US and the other two from the UK and Europe respectively. Prices were range-bound compared to last week. Scrap importers in Turkiye were still looking for March shipment cargoes, and further bookings are expected.

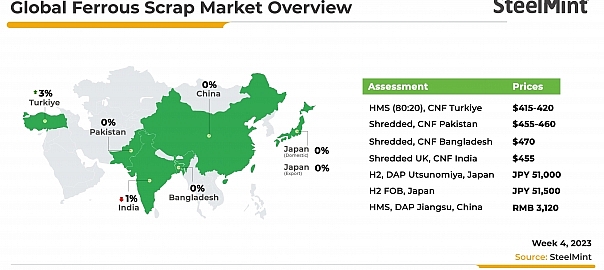

SteelMint’s assessment for US-origin HMS 1&2 (80:20) stood at $418/t CFR Turkiye, up by $8-10/t w-o-w.

Pakistan’s ferrous scrap market on mute: The imported scrap market remained muted for yet another week. The ongoing currency crisis impacted the steel industry severely. The government has restricted the opening of any new LC except for essential items.

Industry experts believe that major mills have the material in hand but are only able to continue their work gradually. However, if the LC issue is not resolved, the industry will continue to suffer.

Mills increased their rebar prices by over PKR 25,000/t ($100/t) exw due to the material shortage and increased cost of production.

SteelMint’s assessment for imported shredded scrap in container stood at $458/t CFR, down by $3/t w-o-w.

Bangladesh market extends silence w-o-w: The imported scrap market was largely quiet over the last few weeks amid tight liquidity issues even as mills are running out of adequate scrap stocks along side limited demand for finished steel.

Overseas bulk offers existed but buyers were resisting amid the current market scenario. Mills were taking each step with caution in concluding deals of any substantial quantity, informed one of the well-known end-users based out of Chattogram.

Fresh offers for US-origin bulk HMS were at $445-450/t CFR Chattogram, lower by $5/t.

The container market in Bangladesh has been largely quiet throughout the month. The market witnessed negative sentiments on limited trading activities because of the LC opening issue.

SteelMint’s assessment for shredded scrap in containers stood at $470/t CFR, stable w-o-w.

India’s scrap market awaits budget 2023: Indian steel industry players were mostly quiet this week, with limited quantity deals heard from Middle East-originated suppliers. Steel producers were waiting for the upcoming financial budget, which is scheduled on 1 February. Interestingly, market players kept their eyes on global market activities, as prices moved up in recently concluded deals from Turkish buyers.

However, suppliers were cautious and tried to sell their material at increased prices to Turkish and Indian buyers, in the absence of scrap buyers from Pakistan and Bangladesh. Prices remained high due to low scrap generation and material scarcity.

SteelMint’s assessment for UK-origin shredded was at $455/t CFR, down by $5/t w-o-w.

Vietnam’s scrap market sentiment stable; offers high: Imported scrap market activities in Vietnam remained gloomy at the beginning of the week, following the stable sentiment and market participants being out of the market due to the holidays.

Imported scrap offers were mostly high as both suppliers and buyers were out of the market and showing less interest due to the ongoing holidays.

Offers for Japanese bulk H2 scrap remained at $445/t CFR Vietnam, up by $15/t w-o-w.

Bulk offers for the mix of HMS 1&2 (80:20) and shredded scrap from the US were heard at $455/t CFR, up by $15/t w-o-w.

Japan’s scrap export prices stable w-o-w: Japan’s scrap export prices were mostly stable throughout the week. Trade was muted due to the absence of active buyers in the market due to the Tet holidays. Meanwhile, China’s scrap and futures markets were closed amid the Lunar New Year holidays.

SteelMint’s assessment for Japanese H2 scrap export prices stood at JPY 51,500/t ($397/t) FOB, unchanged w-o-w.

Leave a Reply