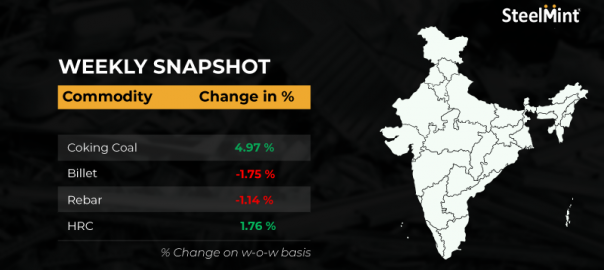

The domestic steel market witnessed a downward trend during the week 3 (16 Jan- 21 Jan’23). Semi-finished steel prices plunged in the range of INR 50-1,450/tonne (t). Domestic induction furnace finished longs offers saw a negative trend, decreasing up to INR 1,300/t w-o-w. Whereas trade reference prices for hot-rolled coils (HRCs) and cold-rolled coils (CRCs) increased in the range of INR 100-1,500/t across regions.

Iron ore and pellets

- SteelMint’s bi-weekly domestic pellets (Fe 63%) index, PELLEX, stood at INR 10,250/t DAP Raipur, down marginally by INR 100/t compared to the last assessment on 17 January. 35,000 t of deals were reported in the last publishing window.

- India’s top iron ore miner, NMDC, conducted an auction for 600,000 t of iron ore (both fines and lumps) from its Donimalai mines in Karnataka on 18 Jan’23. The auction received a good response with the entire quantity getting booked. According to sources, 120,000 t of lumps (10-40mm, Fe61% Indicative) and 80,000 t of fines (Fe59% Indicative) were booked at base prices of INR 3,174/t and INR 2,464/t, respectively.

- India’s pellets export trade remained largely stable compared to last week. SteelMint’s India pellet (Fe 63%, 3% Al) export index, FOB east coast, was assessed at $118/t, inching up by $1/t w-o-w. The market remained silent as most participants are out for Lunar New Year celebrations.

- State-owned Odisha Mining Corporation (OMC) held an iron ore auction on 17 Jan’23. 316,000 t, or 79.2% out of 399,000 t of lumps put up for auction, received bids, while 587,000 t of iron ore fines, or 90.44% of the total quantity of 649,000 t, received bids.

- JSW Steel conducted an auction for 205,400 t of iron ore lumps from Odisha on 16 Jan’23. 102,700 t of lumps (Fe61%, 10-40) were booked at the floor price of INR 5,700/t from Nuagaon mines. And, 102,700 t of lumps (Fe61%, 10-40) were booked at INR 6,210/t against the floor price of INR 5,700/t from Narayanposhi mines. Prices include royalty, DMF, and NMET charges.

Coal

- Australian hard coking coal prices increased by $16/t w-o-w to $325/t FOB and $338/t CNF India as heavy rainfall in the Queensland region led to supply constraints. Shipments from major ports were affected due to operational disruptions.

- Prices of South African RB3 (4800 NAR) thermal coal at Vizag Port fell by INR 300/t w-o-w to INR 11,500/t ex-port.

- RB1 (6000 NAR) grade prices came down marginally to $171/t FOB while RB3 prices were assessed at $125/t CFR India.

Ferrous scrap

- Indian imported scrap buyers were active in the market, however, limited deals were concluded throughout the week. Prices were mostly stable at $455-460/t levels as buyers slowed down fresh bookings due to bulk cargo arrivals.

- However, mills booked many small slots from Middle Eastern-based suppliers.

- SteelMint’s assessment for the UK-origin shredded scrap stood at $460/t CFR Nhava Sheva, unchanged w-o-w.

Ferro alloys

- Silico manganese prices fall by 2% w-o-w to INR 78,200 exw Durgapur and INR 78,900/t exw Raipur. Prices fell as a result of local demand declining, deteriorating liquidity issues, a negative international market, and worsening domestic liquidity issues.

- Ferro manganese fell marginally by 1% w-o-w to INR 79,400/t exw-Durgapur and INR 79,800/t exw Raipur due to restricted demand for special steel and the imbalance between supply and demand.

- Ferro chrome prices rose by INR 2,700/t w-o-w to INR 110,300/t exw-Jajpur due to good export demand. Production cuts amid electricity curtailment in South Africa and Zimbabwe also supported India’s ferro chrome prices.

- Some ferro silicon producers in Bhutan offered at around INR 125,000/t exw, while Guwahati-based producers offered in the range of INR 120,000-125,000/t exw. Bhutan’s producers received adequate inquiries from the European market. This also influenced smelters to increase their offers and Guwahati’s producers followed the suit.

Semi-finished

- Indian semis trade slowed down this week and prices slumped by INR 50-1,450/t amid declining inquiries of finished products in the major markets. Domestic billet prices decreased by INR 300-1,450/t while sponge manufacturers also reduced offers by INR 50-800/t, w-o-w.

- SAIL-Bhilai Steel Plant (BSP) conducted an auction for 5,700 t (60 kg and 52 kg, full length) of commercial rails on 17 Jan’23. Only 850 t of material was booked and the remaining quantity remained unsold due to a high base price.

- SAIL-Rourkela Steel Plant (RSP) held an auction for 700 t of steel grade pig iron on 17 Jan’23. The entire quantity was booked in the range of INR 43,400-43,500/t exw.

- Tata Metaliks raised pig iron (both basic and foundry grades) prices by INR 1,500/t ($18t). Post-revision, offers for foundry grade stood at INR 49,500/t and basic grade (Si 1.0-1.5%) at INR 46,500/t. Prices are exw-Kharagpur and applicable for Kolkata and Howrah markets.

Finished longs

India’s induction furnace-route finished long steel market observed subdued buying inquiries at higher offer prices throughout the week in major supplying regions. Due to a lack of interest from buyers’ side at such high offers, the fluctuating price trend was evident this week. Traders resorted to need-based buying on hopes of price correction which forced manufacturers to give trade discounts or reduce offers marginally following the raw material price trend.

- On a w-o-w basis, rebar steel prices declined in the range of INR 200-1,300/t in northern, eastern and central Indian markets while in southern and western regions, prices increased by up to INR 600/t.

- Trade reference prices of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size were assessed at INR 51,700-52,100/t exw-Raipur and INR 56,700-57,200/t exw-Jalna.

- Trade discounts given by Raipur- based heavy structural steel manufacturers were at INR 2,200-2,500/t and trade reference prices of 200 mm angles stood at INR 58,000-58,500/t exw-Raipur.

- Trade discounts in Raipur wire rod given by resellers stood at over INR 1,000/t and trade reference prices at INR 51,200-51,700/t exw-Raipur and INR 51,800-52,200/t exw-Durgapur, size 5.5 mm.

- Trade level prices of BF-route rebars saw a sharp rise w-o-w by INR 1,000-1,400/t across major markets. Prices in the trade market touched 6-month high levels as primary mills announced hike in list prices by up to INR 1,500/t this week. Restocking demand in the distribution channel coupled with the shortage of inventories of specific sizes continued to weigh on the supply-demand scenario.

- Rebars (12-32 mm, BF-route, IS 1786, Fe500D) prices increased by INR 1,400/t w-o-w to INR 60,900/t, exy-Mumbai, excluding GST at 18%.

Finished flats

- Trade reference prices of flat steel products have been on a rally since 21 December 2022. Major mills took an interim hike in their flat steel list prices earlier this week. Increasing raw material costs and decent export bookings were the reasons behind the price hikes by mills. This also resulted in higher quotes in the traders’ market.

- Improved performance reports of the automobile industry and better demand from white goods and infrastructure helped easing of inventories with the mills, sources informed. This is likely to keep the trade level prices buoyed in the near term.

- On the exports front, SteelMint’s HRC (SAE1006) export index increased by $18/t w-o-w tp $633/t FOB east coast this week. Global market sentiment improved as buyers in the Middle East and European markets were coming up with requirements and a few deals were recorded in January.

- Indian mills could face less competition in the market, with the Chinese mills having exhausted their export allocations for March shipments, hinted a reliable EXIM market source. Chinese mills are likely to come up with higher offers post the Lunar New Year holidays for April 2023 deliveries- another booster to the global market sentiments, he added.

Leave a Reply