- Finished steel exports also stable y-o-y in 2022

- Exports likely to fall y-o-y in 2023

- CBAM to impact exports from developing countries

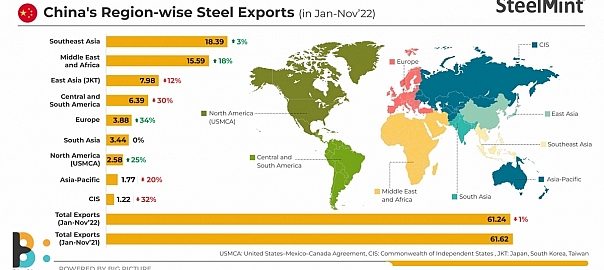

Morning Brief: China’s steel exports in January-November, 2022 were recorded at 61.24 million tonnes (mnt) — down a marginal 1% against 61.62 mnt seen in the same period last year, as per Customs data maintained with SteelMint.

Data shows that although Southeast Asia retained its status as the leading importing geography, the growth rate rose a very nominal 3% y-o-y. On the other hand, exports to the Middle East & Africa have been gaining prominence.

In calendar 2022, China’s finished steel exports totalled 67 mnt, up a negligible 0.9% y-o-y, indicating that volumes were stable, due to subdued home consumption. The country’s finished steel imports dropped 26% y-o-y to 11 mnt, again denoting dipped home demand.

But China has indicated it aims to reduce commercial grades sales overseas and concentrate on value-added, high margin special steel. The Russia-Ukraine war and then Covid provided a one-off opportunity to export to offset the lack of home demand. Thus, although volumes were expected to drop 5-7 mnt in 2022, they did not. In fact, exports ballooned over May-August, 2022, especially because of the war and later, due to Covid. In fact, seen quarter-wise, exports averaged 20.30 mnt in April-June, 2022 — a period after the war. Then dropped to 17.80 mnt over July-September, and dipped further to 16.17 mnt in October-December last year as global demand was pressured by inflation and sliding currencies.

Click here to download China’s country-wise steel exports

Middle East and Africa

China’s steel exports to the Middle East and Africa rose 18% over January-November, 2022. This geography is emerging as an important export destination for China, as it grapples with a real estate market crisis, unprecedented Covid surges, and policy-driven production cuts with an eye on its decarbonisation goals.

However, data reveals that the 18% increase is lesser than the 23% rise recorded in January-October, 2022 or even 22% in January-September, 2022.

But, overall, heightened infrastructure development activity in Middle East is warranting this extra procurement from China.

The Covid-19 pandemic severely affected the construction industry and associated equipment demand across the Middle East and Africa in 2020. This was primarily attributed to disruptions in the supply chain, reduced investment in new equipment procurement, halt and postponement of construction projects, and unstable economic growth of many countries in this geography. However, since 2021, the construction industry across the Middle East and Africa has been witnessing significant investment growth, which is likely to drive the market in future. Rising government investments in infrastructure development in the Middle East and Africa — in Saudi Arabia, Kuwait, Oman, the United Arab Emirates, and Egypt – are propelling steel demand and end-users are looking at China’s competitive export offers, which declined from a 3-month average of $813/tonne FOB in April-June, 2022 to $576/t FOB in Q4.

South East Asia

South East Asia, although it retained its top spot as China’s leading export destination, saw volumes increasing by a nominal 3% to 18.39 mnt over January-November, 2022 compared to 17.79 mnt in the year-ago period.

Vietnam’s volumes dipped -3% y-o-y to 5.12 mnt in the period under review against 5.26 mnt in the corresponding period last year

Vietnam’s slow post-Covid recovery, dipping demand, and preference for domestic material slowed imports, forcing the country to become an exporter itself for the last few months.

Inflation and liquidity tightening by other Southeast Asian governments are also keeping demand lower and imports somewhat range-bound.

Outlook

China’s crude steel production is expected to drop in 2023 but consumption will possibly rise marginally. This scenario, along with a waning emphasis on commercial grades – thanks to environmental issues — will likely lead to a y-o-y drop in China’s steel exports in the current calendar.

Also, the European Union’s carbon tax policy will impact China’s steel exports in the long term. It may be recalled, in July 2021, the European Commission adopted a proposal for a carbon border adjustment mechanism (CBAM) in line with its goal to cut carbon emissions by 55% by 2030. The CBAM will tax imported goods sold in EU markets on the basis of their carbon content (the emissions required to produce them), which depends on their material and energy inputs.

While this measure will help the EU reduce carbon emissions, it will negatively impact steel exports from developing countries such as China or even India. Challenges like rising steel export costs to the EU, shrinking price advantages, and declining product competitiveness will rear their head but eventually usher in an era of green steel manufacturing. As per the EU’s revised emissions trading system (ETS), segments covered by these norms will have to reduce their emissions by 62% by 2030 compared to 2005. Steel falls within its ambit.

CBAM will be implemented from October, 2023.

Leave a Reply