China’s spot thermal coal prices have been on the upward since early last week, but at the same time, coal stockpiles maintained high at northern ports, which indicates a weaker demand.

The logic seems contradictory but we still find some factors behind.

Coal stockpiles at northern transfer ports increased sharply on a year-on-year basis. In the first few days of this year to January 10, the combined stocks at the three ports (Qinhuangdao, Jingtang and Caofeidian) kept staying above 22 million tonnes, compared with 18-19 million tonnes over the same period of 2022.

At Qinhuangdao alone, coal stocks were 5.5 million tonnes as of January 10, compared with 4.3 million tonnes on the same day of 2022, making a 28.4% rise.

There are two factors behind the elevated stockpiles. On the one hand, rail transport has improved to normal level thanks to weakened impact of the epidemic, evidenced by a 15% rise in rail inflows to northern ports. On the other hand, there was a decline in outflows, due partly to utilities’ delayed shipments of coal under medium- and long-term contracts, partly to traders’ reluctance to sell costlier cargoes they have in hand.

The stock accumulation suggests weakened demand. Some utility sources said they could still satisfy demand during and after the Chinese New Year holiday without spot purchases.

At the same time, the price increase is mainly related to stock-building requirements and the expectation of the near-term temperature drops.

Fujian asked all power plants to keep coal stockpiles above 15 days of use in the first quarter this year, and there will be a widespread drop of 5-20 degree Celsius in many parts of the country amid a cold spell moving southward.

Views divergent on market trend

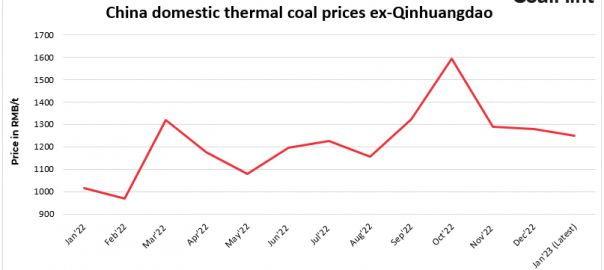

On January 11, the benchmark 5,500 Kcal/kg NAR thermal coal was offered at 1,230-1,250 yuan/t FOB with VAT at northern ports, about 10 yuan/t higher than a day ago, adding to a 50 yuan/t rise since the beginning of this upswing on January 5.

Cargoes of 5,000 Kcal/kg NAR were mainly offered at 1,090-1,100 yuan/t FOB, compared with 1,050 yuan/t on January 5. The 4, 500 Kcal/kg NAR grade also gained 30 yuan/t over the period.

On the market trend in January-February, opinions are divergent, with most participants believing the momentum would be depleting soon, citing high stockpiles at power plants and high contract delivery rate. A few participants, however, argued the temperature drop would push up coal consumption, forcing some small-sized plants to buy prompt spot coal.

There are still some participants cautioned uncertainty of the market, which mainly depends on the economic performance. Yet, some cement producers expressed optimism, noting the peak of COVID infections has passed and most cities have returned to the normal.

Some buyers abandoned the purchase idea after inquiring as they thought the price was rising too fast recently with no significant support from the fundamentals.

Meanwhile, thermal coal prices in major producing areas rose steadily. As a number of coal mines stopped operation for the Lunar New Year holiday, the overall production has shrunk. Mines still in operation took the opportunity to increase prices.

According to a survey by Sxcoal on 20 coal mines located in Shanxi, Shaanxi and Inner Mongolia, 12 mines raised prices in a range of 10-60 yuan/t, five suspended for holiday and three maintained prices stable.

The increase pushed up the cost of shipments to northern ports, which also partly contributed to the portside price increase. Some traders thus intended to hold back their remaining inventories to sell after the Lunar New Year celebrations.

Note: This article has been exchanged under the article exchange agreement between CoalMint and Sxcoal.

Leave a Reply