The global ferrous scrap market has remained active after the New Year holidays. Turkish buyers raised the market momentum with a flurry of deals at higher prices. Japan’s export prices remained steady and this month’s Kanto tender outcome is awaited. Tokyo Steel’s prices remain unchanged since 14 December 2022 as are China’s Shagang Steel’s bids for scrap since 30 December. However, major South Korean mills have raised purchase prices by $16/t.

The South Asian market, in comparison, has been relatively slow with only Pakistani buyers being active, whereas Indian buyers have inked limited deals – a few containerised and one bulk deal. The Bangladesh market continues to remain silent on LC opening issues.

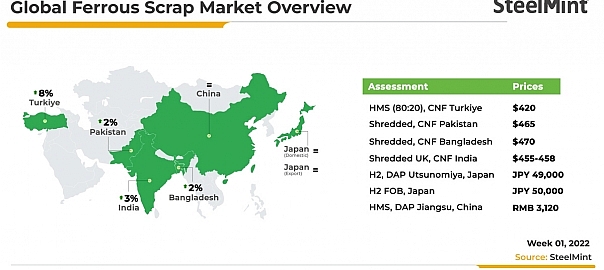

- Buying frenzy in Turkish market: After market participants resumed buying after the holidays, imports of scrap in Turkey increased. Prices continued to rise as supply remained constrained. Prices increased quickly with frequent deals from the US, Europe, and the Baltic region.

A mill based in the Mediterranean region booked a bulk cargo for February shipment which comprised 22,000 t of HMS (90:10) and 5,000 t of P&S. It was booked at $426/t and $441/t CFR respectively.

Imported scrap prices increased significantly by over $30/t w-o-w in recent trades. SteelMint’s daily assessment for HMS 1&2 (80:20) from the US stood at $420-22/t CFR Turkey.

- Bangladesh still silent: Imported scrap trades still remain absent in Bangladesh. Due to LC opening limits, the market has witnessed a slowdown over the last four months. In the past two months, the nation’s imports of bulk scrap have decreased.

Indicative bulk offers to Bangladesh for US-origin HMS are at $450/t CFR, up significantly by $15-20/t w-o-w after the Turkish deal.

Fresh containerised offers for UK-origin shredded scrap are at $470/t CFR, up $10/t w-o-w. However, no deals were reported. - Pakistani buyers active lately: Buyers began making purchases later this week, and due to restocking activities, prices may briefly trend upward by $10–$15/t due to limited overseas offers during the winter holidays and the typically slow accumulation rate of scrap. Pakistan’s imported scrap market remained active throughout the week.

SteelMint’s assessment for shredded scrap in containers stands at $460-465/t CFR, up $15/t w-o-w. Prices are at a four-month high.

Around 14,000 t containerised shredded scrap has been booked throughout the week at a price range of $445-465/t.

- Indian import prices rise: Indian mills remained active as activities in the market resumed after the winter holidays. However, imported scrap prices continued to move up on the back of increased enquiries from buyers and active deals concluded by Turkiye.

Meanwhile, a Kandla-based mill booked a 40,000 t bulk scrap cargo from the US at $450/t CFR for early-February shipment. Many deals have been recorded for containerised material.

SteelMint’s assessment for Europe-origin shredded was recorded at $455-458/t CFR, up $10/t w-o-w.

- Japanese export offers likely to rise: Japan’s scrap prices continued to be largely stable at the beginning of the New Year. Trade remained slow in the absence of active enquiries from buyers this week. Japanese traders expect scrap demand from South Korea and Taiwan to improve in the near term.

Japanese material could see price hikes as scrap availability is likely to be limited due to slower supply in response to growing domestic demand.

SteelMint’s assessment for Japanese H2 scrap export prices stands at JPY 50,000/t ($372/t) FOB, stable w-o-w.

Prices of overseas material rose by around $10-15/t, while local scrap prices inched up owing to tight supply.

- Vietnamese market sluggish: Due to inactive trade channels, the Vietnamese scrap market was largely quiet last week. Local mills concentrated on buying domestic scrap at lower prices. Due to limited supplies, prices of local scrap increased marginally while material from abroad was costlier by $10–15/t. Buyers are waiting for Japan’s Kanto scrap export tender scheduled for 12 January.

Assessments for US-origin bulk offers are now at $410-415/t CFR, up $10-15/t w-o-w. SteelMint’s assessment for Japanese H2 material is at $400-410/t CFR, an increase of $10/t on-week.

Leave a Reply