- Induction mills feel cost heat

- HRC producers hemmed in by global demand slump

- Trend may sustain for some time

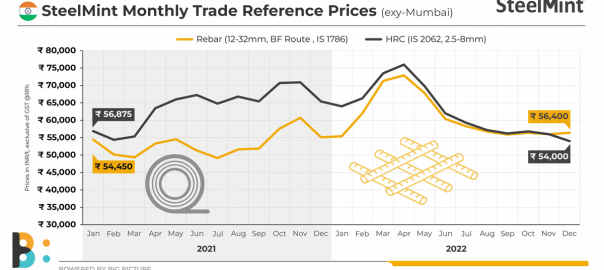

Morning Brief: India’s rebar prices have overshot hot rolled coil (HRC) prices by a record INR 2,400/tonne (t) after a gap of almost three years. HRCs traditionally command a price higher globally compared to rebar and this trend is replicated in India too. However, in December, 2022, as per data maintained with SteelMint, the average monthly price of rebar was at INR 56,400/tonne (t) ($682/t) while HRC slid down to INR 54,000/t ($653/t). The last time rebars were more expensive than HRCs was in March 2020, at -INR 2,250/t ($27/t). It may also be mentioned the spread had hit an all-time high, at nearly INR 16,000/t ($192/t) in June 2021.

Why have rebar prices spiked?

In India, 60-65% of the longs market is commanded by the coal- and power-intensive induction furnace (IF) mills. Mostly all their input materials have become costlier, raising the cost of production.

1. High coal costs: Last year saw IFs’ cost of production escalating with the runaway inflation in coal. Imported South African RB2 (5500 NAR) grade coal prices catapulted by a massive 102% y-o-y in 2022 to nearly INR 18,000/t ($218/t) against INR 9,000/t ($109/t) in the preceding year.

Coal prices escalated because of the changed trade flows post-the Russia-Ukraine war. The western world’s sanction on Russia included a ban on procuring its coals. Plus, energy politics pushed up gas prices. Utilities in the European Union, hedged in by record high gas prices, turned to buying thermal coal from South Africa which diverted material to the EU, leaving traditional buyers like Indian sponge units with no choice but to accept expensive coal.

Around 56% of India’s steel industry produces through the thermal coal-intensive EAF-IF route and within the sponge iron producers, 80% undertake coal-based production. Sponge iron is a key feed for the IF mills, whose cost also rose 15% y-o-y last calendar.

2. Higher power tariffs: That apart, prices of domestically auctioned coal from SECL rose to touch over INR 9,000/t in May’22 from INR 5,000/t ($60/t) levels seen earlier last year, raising the cost of captive power as well as that bought from discoms. Overall, imported coal became more expensive, pushing up the cost of power generation for utilities which blended imported coal.

As per IEX, the monthly average spot electricity prices in the day-ahead-market platform rose 46% to INR 5.77/unit in 2022 as against INR 3.94/unit in CY21. This price is not specific to the industrial sector but assessed for all customers as a whole but gives an indication of the kind of increase in power tariffs Indian consumers experienced last year.

3. Costlier and scarce scrap: Scrap, another feed, was in short supply and costlier by almost 18% last year compared to 2021. The government’s crackdown on unaccounted transactions to bring more unorganized players within the GST ambit led to lesser scrap generation and collection in local markets, especially in northern India.

Why is HRC trading at a discount to rebar?

1. Global demand downtrend: Global flats prices had corrected a few months back because of lack of demand and recessionary trends brought about by high energy and gas prices and sliding currencies. Since most flat products are manufactured by the BF-BoF route, mills were unable to stop production. This led to inventory pile-up amid lack of demand and resulted in a drop in prices. Indian mills too had to keep prices down in tandem with global trends.

2. Imports pressure domestic prices: Because of the inventory pile-up, many producers turned exporters, like Vietnam and Japan. Cheap HRCs found their way into India, forcing primary mills to keep their domestic HRC prices in check as landed imported tags became cheaper by almost INR 8,000/t at a juncture.

3. Export tax impact: Around 20% of India’s steel was exported last fiscal, indicating that the country has considerable exposure in overseas markets. The slump in demand, even from non-EU countries, and the 15% export tax were a double whammy. This 20% that could have been exported remained within the country but found few takers.

Outlook

Globally, markets are opening up and prices increasing, which is encouraging mills to explore exports at higher offers. Europe looks good currently. Thus, HRC prices are likely to regain lost ground.

But rebar prices will continue to remain high, at least for another month, because the cost pressure on IFs will not ease soon. Sponge iron production from Odisha will be reduced in January because of the hockey World Cup tournament which will keep prices of the material elevated.

Moreover, in China too rebar prices are playing catch-up with HRC because of the cost push which will be reflected in India too.

Leave a Reply